The UKPF Retirement Flowchart: Interactive Guide with Real Projections

The UKPF Retirement Flowchart: Interactive Guide with Real Projections

The r/UKPersonalFinance retirement flowchart is one of the UK's most trusted resources for financial planning. It's a simple, logical sequence: emergency fund → employer match → debt → ISAs → extra pension contributions.

But a flowchart doesn't show you the numbers. How much will that employer match actually be worth at retirement? What happens if you prioritise ISAs over pensions? How does early debt repayment change your wealth trajectory?

This guide walks through the UKPF flowchart step by step, with real projections using PoundSense's pension calculator. See exactly how each decision affects your retirement.

The UKPF Flowchart: A Quick Overview

The flowchart follows this priority order:

- Emergency fund (3-6 months expenses)

- Get your employer pension match (free money)

- Pay off high-interest debt (>4-5% interest)

- Max your ISA allowance (£20,000/year, tax-free, flexible)

- Increase pension contributions (tax relief up to £60,000/year)

- Other investments (taxable accounts, property, etc.)

Each step builds financial stability before moving to the next. Let's walk through it.

Step 1: Build Your Emergency Fund (3-6 Months)

Why it comes first: Life happens. Boiler breaks. Car needs replacing. Redundancy. Without savings, you'll rely on credit cards or — worse — early pension withdrawals (25% penalty before age 55).

How much: 3-6 months of essential expenses (rent/mortgage, bills, food, transport). Not your full salary — just enough to survive a rough patch.

Where to keep it: Easy-access savings account. Not invested. Not in a pension. Instant access, no risk.

Interactive step: Use our pension calculator to see how much you'll save later. But this step isn't about returns — it's about security.

Step 2: Get Your Full Employer Pension Match

Why it's second: Free money. If your employer matches 5% and you contribute 3%, you're leaving 2% on the table. Over 30 years, that's tens of thousands of pounds lost.

Example: You earn £40,000. Your employer matches up to 5% (£2,000/year). You contribute 3% (£1,200). You're missing out on £800/year of free contributions.

Interactive projection:

👉 See the impact of employer match →

Try adjusting the contribution rate from 3% to 5%. Watch your retirement pot jump by £50,000+ (assuming 5% real returns over 32 years).

Key insight: Employer match is the highest-return "investment" you'll ever make. It's an instant 100% gain.

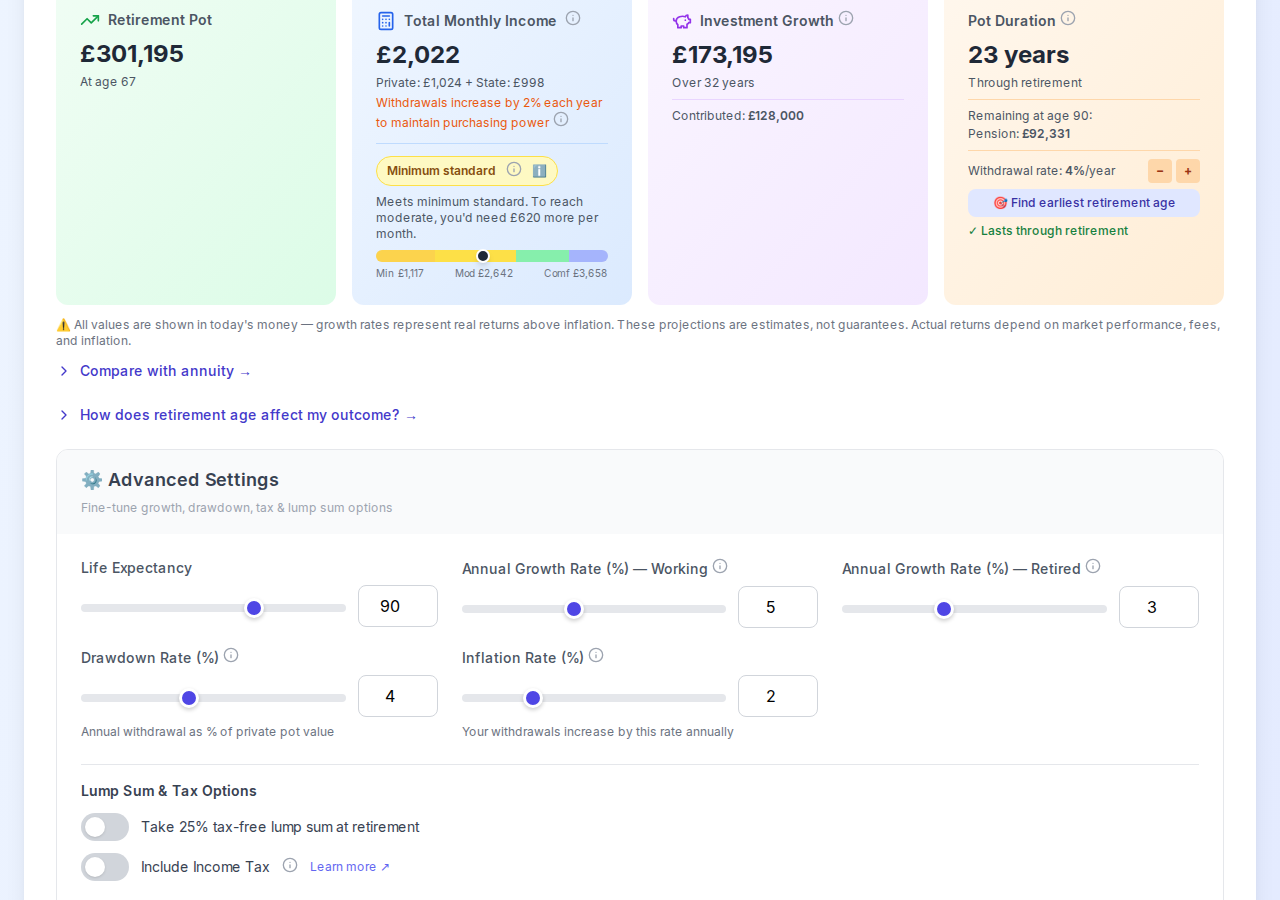

Example projection: 35-year-old on £40,000 salary with 5% employee + 5% employer contributions = £301k pot at age 67.

Example projection: 35-year-old on £40,000 salary with 5% employee + 5% employer contributions = £301k pot at age 67.

Step 3: Pay Off High-Interest Debt (>4-5%)

Why it's third: Debt above 4-5% costs more than you'll earn investing. Credit card at 19.9%? You'd need 20%+ annual investment returns to break even — impossible without extreme risk.

What counts as "high-interest":

- Credit cards (15-25% APR)

- Personal loans (5-15% APR)

- Car finance (6-12% APR)

- Store cards (20-30% APR)

What doesn't:

- Mortgage (typically 3-5%)

- Student loans (RPI + 0-3%, income-contingent)

Interactive step: Use our lump sum calculator to model debt vs investing. See when it makes sense to pay off a loan early vs investing the cash.

👉 Compare debt repayment strategies →

The lump sum calculator models debt repayment vs investing side-by-side with real UK tax treatment.

The lump sum calculator models debt repayment vs investing side-by-side with real UK tax treatment.

Step 4: Max Your ISA Allowance (£20,000/Year)

Why ISAs before more pension: Flexibility. Pensions lock money away until age 55 (rising to 57 in 2028). ISAs are accessible anytime, tax-free, no restrictions.

When to prioritise ISAs:

- You might need the money before retirement age

- You're already contributing enough to your pension (e.g. 15%+)

- You're a higher-rate taxpayer and want tax-free growth without lifetime allowance worries

When to skip straight to pensions:

- You're confident you won't need the money before age 55

- You're a higher-rate (40%) or additional-rate (45%) taxpayer (tax relief beats ISA tax-free growth)

Interactive comparison:

👉 Compare ISA vs extra pension contributions →

Try enabling "ISA contributions" and see how accessible savings compare to locked-away pension pots.

Read our pension vs ISA comparison for a deeper look at which wrapper suits your situation.

Step 5: Increase Your Pension Contributions

Once your ISA is maxed (or you've decided pensions are a better fit), increase pension contributions beyond the employer match.

Why more pension:

- Tax relief: 20% basic rate, 40% higher rate, 45% additional rate. Every £100 you contribute costs you £60 if you're a higher-rate taxpayer.

- Tax-free lump sum: 25% of your pot (up to £268,275) is tax-free at retirement.

- No capital gains tax inside the pension wrapper.

How much can you contribute?

- Annual allowance: £60,000 (or 100% of earnings, whichever is lower)

- Lifetime allowance: Abolished in 2024 (replaced by lump sum limits)

Interactive projection:

Try increasing the contribution rate from 10% to 20%. See how an extra £6,000/year (costing you £3,600 after higher-rate relief) adds £200,000+ to your pot over 27 years.

Step 6: Other Investments (Post-Pension, Post-ISA)

What's left? Once you've maxed pensions (£60k/year) and ISAs (£20k/year), you're saving £80,000+ annually. Most people never reach this step.

Options:

- Taxable brokerage accounts (General Investment Accounts) — capital gains tax applies (£3,000 annual exemption as of 2024/25)

- Property investment (buy-to-let, holiday lets)

- VCTs / EIS (high-risk, tax-advantaged venture capital)

- Premium Bonds (tax-free, but returns are lottery-based)

Interactive step: N/A. This is beyond the scope of pension modelling. Consult an IFA if you're at this level.

Real-World Example: Following the Flowchart from Age 30 to 67

Profile:

- Age: 30

- Salary: £45,000

- Employer match: 5% (if you contribute 5%)

- Current pension pot: £10,000

- Goal: Comfortable retirement at 67

Year 1-2: Build Emergency Fund

Save £10,000 in easy-access savings (6 months expenses). No investing yet.

Year 3-35: Follow the Flowchart

- Employer match: Contribute 5% (£2,250/year). Employer adds 5% (£2,250). Total: £4,500/year.

- No high-interest debt.

- ISA: Max £20,000/year (if affordable).

- Extra pension: Increase contribution to 15% (£6,750/year). Employer still adds 5%. Total: £11,250/year.

Projected outcome at age 67:

- Pension pot: ~£800,000 (assuming 5% real returns)

- Annual income: ~£32,000/year (4% withdrawal rate + State Pension)

- Tax: ~£3,500/year (20% basic rate on drawdown above personal allowance)

Result: Comfortable retirement, PLSA standard met, flexibility from ISA savings.

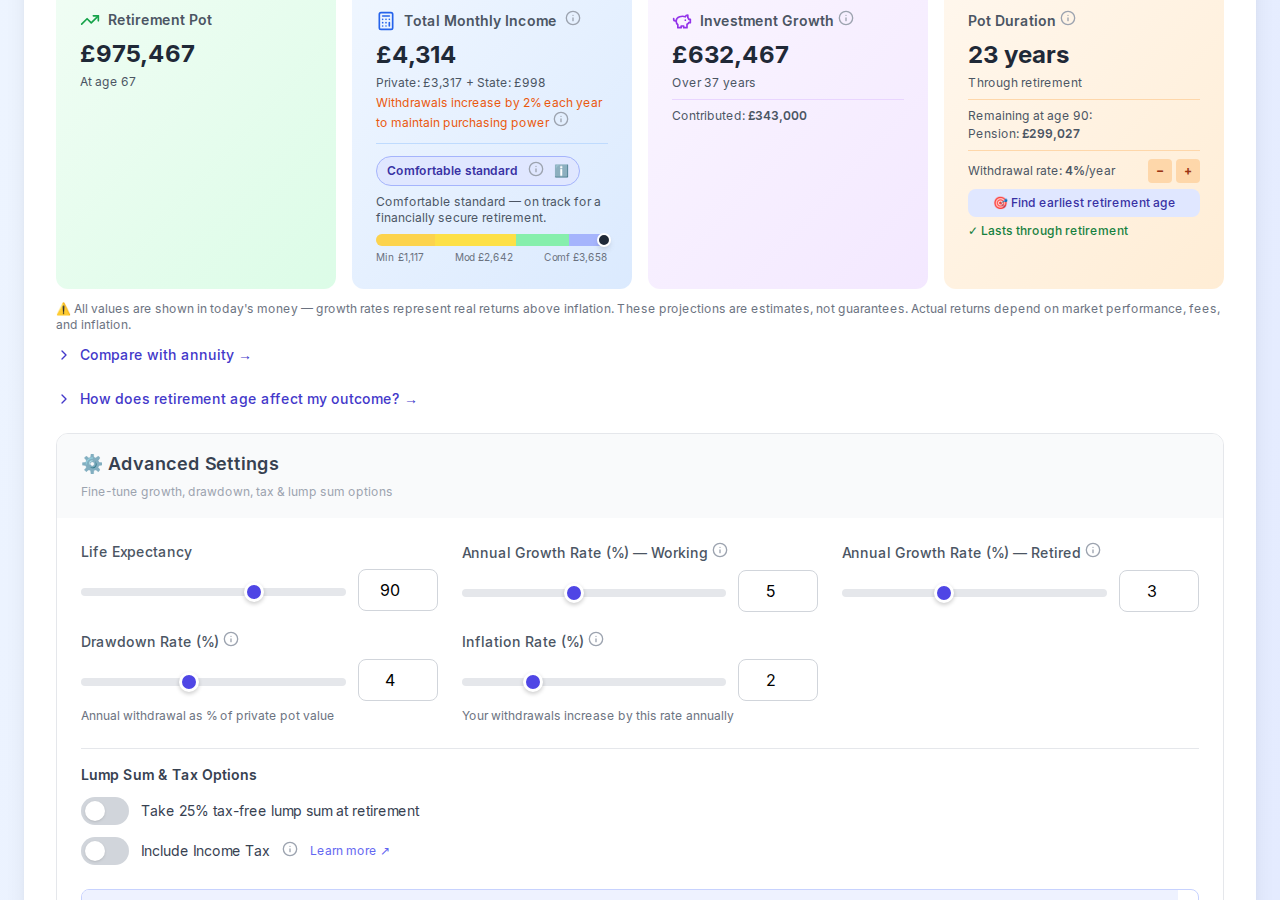

Following the flowchart from age 30: £45k salary, 15% employee + 5% employer contributions, starting with £10k pot = £975k at retirement and £4,314/month income (comfortable standard).

Following the flowchart from age 30: £45k salary, 15% employee + 5% employer contributions, starting with £10k pot = £975k at retirement and £4,314/month income (comfortable standard).

Key Takeaways: The Flowchart in Practice

- Emergency fund first. Boring but essential. No investing until this is sorted.

- Employer match is non-negotiable. Never leave free money on the table.

- Debt above 5% kills wealth. Clear it before investing.

- ISAs vs pensions depends on your timeline. Need money before 55? ISA. Locked away until retirement? Pension.

- Tax relief makes pensions incredibly powerful for higher earners. 40-45% relief beats ISA tax-free growth.

Tools to Model Your Own Path

- Pension Calculator — Full UK pension modelling with tax, State Pension, drawdown strategies, and employer match

- Lump Sum Calculator — Compare debt repayment vs investing

- Provider Comparison — Compare pension fees across 9 UK providers

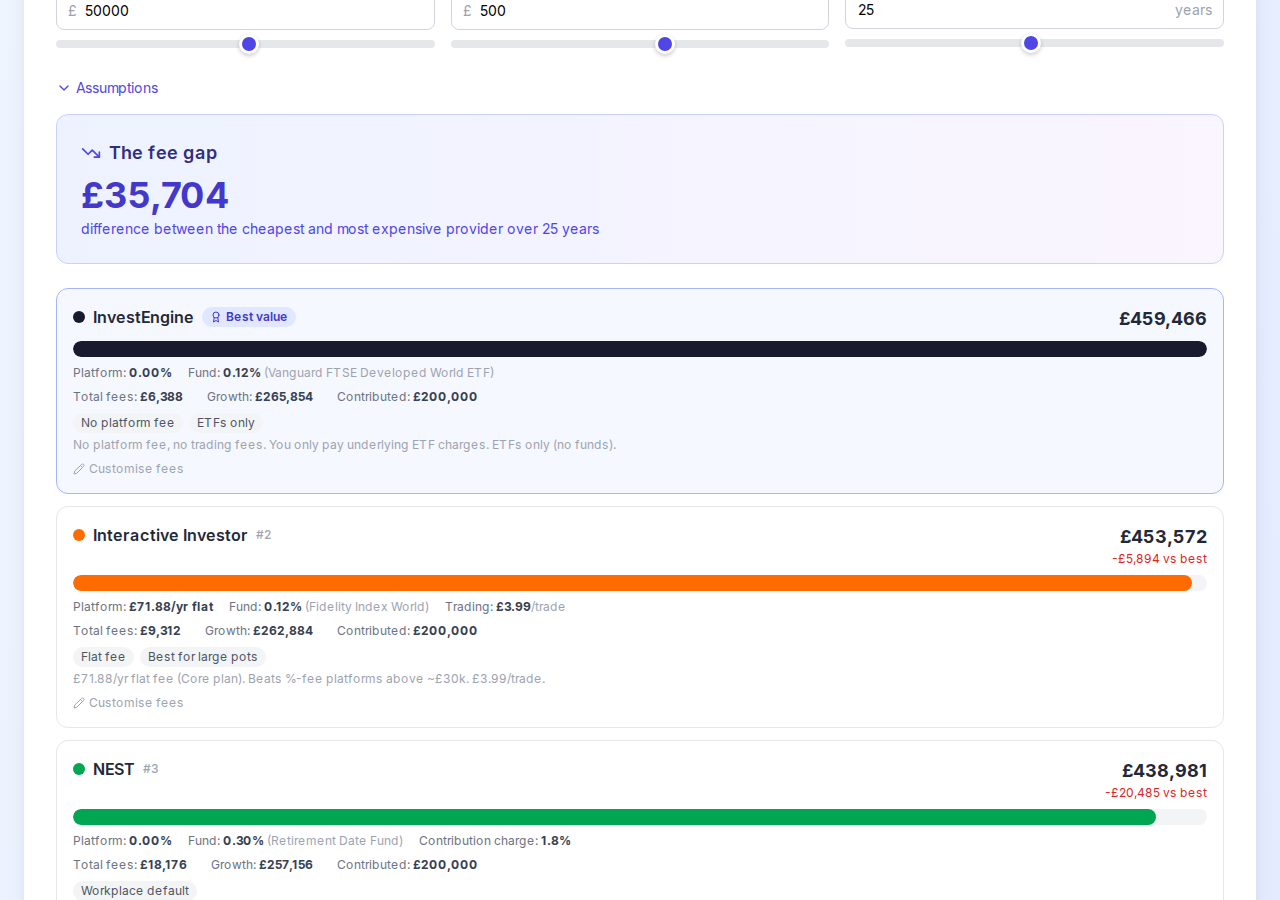

Provider comparison: £35,704 difference between cheapest and most expensive over 25 years on a £50k pot with £500/month contributions.

Provider comparison: £35,704 difference between cheapest and most expensive over 25 years on a £50k pot with £500/month contributions.

Credits & Further Reading

This guide is inspired by the r/UKPersonalFinance flowchart, created and maintained by the UKPF community. It's required reading for anyone serious about UK personal finance.

More from UKPF:

Related PoundSense guides:

- How Much Do You Need to Retire in the UK?

- Pension Drawdown Explained

- SIPP vs LISA: Which Is Right for You?

This guide is for educational purposes only and does not constitute financial advice. Consult an independent financial adviser for personalised recommendations.

Ready to plan your retirement?

Use our free UK Pension Calculator to see how your savings could grow and what your retirement might look like.

Try the Pension Calculator →